LIC New Jeevan Anand Plan - Table No 815

Click here to buy online

CLICK HERE TO INQUIRE

To know the difference between old and New Jeevan anand Plan, Download below Presentation.

| new_jeevan_anand_plan_815_vs_old_jeevan_anand_plan_149.pptx |

Description of New Jeevan Anand Plan - 815

Life Insurance Corporation of India Ltd. Presents,

LIC's New Jeevan Anand Plan is a partaking non-interfaced plan which offers an alluring consolidation of assurance and reserve funds. This mix gives money related assurance against death all through the lifetime of the policyholder with the procurement of installment of lumpsum at the end of the chose policy term if there should be an occurrence of his/her survival. This plan additionally deals with liquidity needs through its loan facility.

1. Benefits:

Death benefit :

Gave all due premiums have been paid, the accompanying death profit might be paid:

· On Death throughout the policy term: death profit, characterized as entirety of "Whole Guaranteed on Death" and vested Straightforward Reversionary Rewards and Last Extra reward, if any, might be payable. Where, "Total Guaranteed on Death" is characterized as higher of 125% of Essential Whole Guaranteed or 10 times of annualized premium. This death profit might not be short of what 105% of every last one of premiums paid as on date of death.

The premiums specified above avoid administration charge, additional premium and rider premiums, if any.

· On death of policyholder whenever after policy term: Fundamental Entirety Guaranteed

Profits payable at the end of Policy Term: Fundamental Entirety Guaranteed, alongside vested Straightforward Reversionary Rewards and Last Extra Reward, if any, might be payable in bump total on survival to the end of the policy term gave all due premiums have been paid.

Support in Benefits : The policy should take part in benefits of the Organization and might be qualified for accept Basic Reversionary Rewards pronounced according to the knowledge of the Partnership throughout policy term gave the policy is in full drive.

Last (Extra) Reward might likewise be pronounced under the plan in the year when the policy results into death case throughout the policy term or due for the survival profit installment gave the policy is in full compel and has run for certain base term.

2. Optional Benefit:

LIC's Incidental Death and Inability Profit Rider: LIC's Unintentional Death and Handicap Profit Rider is accessible as an optional rider by installment of extra premium throughout the policy term. If there should be an occurrence of unintentional death throughout the policy term, Mischance Profit Aggregate Guaranteed will be payable as lumpsum alongside the death profit under the essential plan. If there should be an occurrence of unintentional lasting inability emerging because of mishap (inside 180 days from the date of mischance), a sum equivalent to the Mischance Banquet Whole Guaranteed will be paid in equivalent regularly scheduled payments spread in excess of 10 years and future premiums for Mischance Profit Aggregate Guaranteed and in addition premiums for the parcel of Fundamental Total Guaranteed which is equivalent to Mishap Profit Entirety Guaranteed under the policy, might be waived.

Life Insurance Corporation of India Ltd. Presents,

LIC's New Jeevan Anand Plan is a partaking non-interfaced plan which offers an alluring consolidation of assurance and reserve funds. This mix gives money related assurance against death all through the lifetime of the policyholder with the procurement of installment of lumpsum at the end of the chose policy term if there should be an occurrence of his/her survival. This plan additionally deals with liquidity needs through its loan facility.

1. Benefits:

Death benefit :

Gave all due premiums have been paid, the accompanying death profit might be paid:

· On Death throughout the policy term: death profit, characterized as entirety of "Whole Guaranteed on Death" and vested Straightforward Reversionary Rewards and Last Extra reward, if any, might be payable. Where, "Total Guaranteed on Death" is characterized as higher of 125% of Essential Whole Guaranteed or 10 times of annualized premium. This death profit might not be short of what 105% of every last one of premiums paid as on date of death.

The premiums specified above avoid administration charge, additional premium and rider premiums, if any.

· On death of policyholder whenever after policy term: Fundamental Entirety Guaranteed

Profits payable at the end of Policy Term: Fundamental Entirety Guaranteed, alongside vested Straightforward Reversionary Rewards and Last Extra Reward, if any, might be payable in bump total on survival to the end of the policy term gave all due premiums have been paid.

Support in Benefits : The policy should take part in benefits of the Organization and might be qualified for accept Basic Reversionary Rewards pronounced according to the knowledge of the Partnership throughout policy term gave the policy is in full drive.

Last (Extra) Reward might likewise be pronounced under the plan in the year when the policy results into death case throughout the policy term or due for the survival profit installment gave the policy is in full compel and has run for certain base term.

2. Optional Benefit:

LIC's Incidental Death and Inability Profit Rider: LIC's Unintentional Death and Handicap Profit Rider is accessible as an optional rider by installment of extra premium throughout the policy term. If there should be an occurrence of unintentional death throughout the policy term, Mischance Profit Aggregate Guaranteed will be payable as lumpsum alongside the death profit under the essential plan. If there should be an occurrence of unintentional lasting inability emerging because of mishap (inside 180 days from the date of mischance), a sum equivalent to the Mischance Banquet Whole Guaranteed will be paid in equivalent regularly scheduled payments spread in excess of 10 years and future premiums for Mischance Profit Aggregate Guaranteed and in addition premiums for the parcel of Fundamental Total Guaranteed which is equivalent to Mishap Profit Entirety Guaranteed under the policy, might be waived.

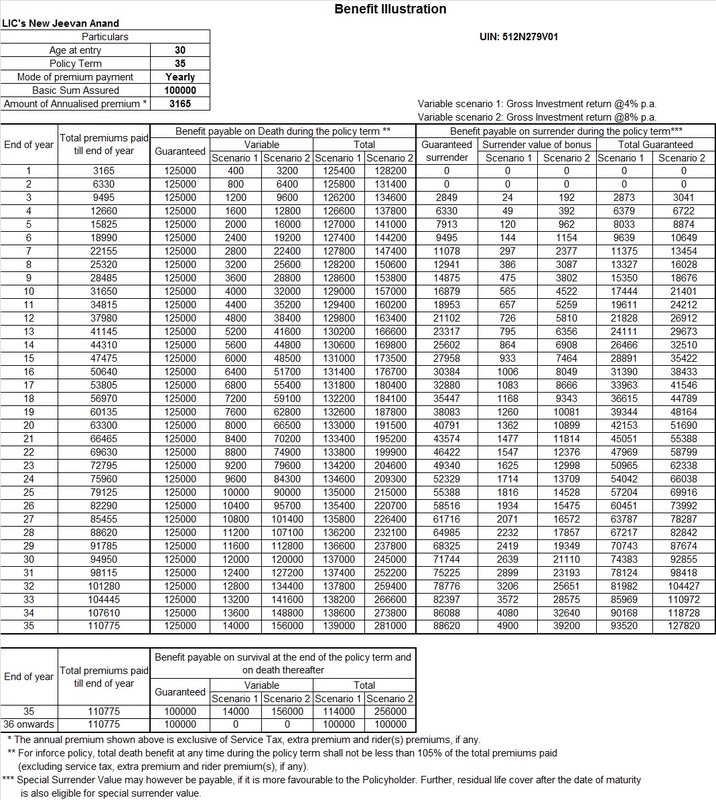

Benefit Illustration:

Statutory cautioning:

"A few profits are ensured and a few profits are variable with profits based for the future execution of your Back up plan carrying on extra security business. In the event that your policy offers guaranteed returns then these will be unmistakably checked "guaranteed" in the delineation table on this page. On the off chance that your policy offers variable profits then the outlines for this page will demonstrate two separate rates of expected future financing returns. These accepted rates of return are not ensured and they are not the upper or lower breaking points of what you may get again, as the estimation of your policy is subject to various components including future financing execution."

Statutory cautioning:

"A few profits are ensured and a few profits are variable with profits based for the future execution of your Back up plan carrying on extra security business. In the event that your policy offers guaranteed returns then these will be unmistakably checked "guaranteed" in the delineation table on this page. On the off chance that your policy offers variable profits then the outlines for this page will demonstrate two separate rates of expected future financing returns. These accepted rates of return are not ensured and they are not the upper or lower breaking points of what you may get again, as the estimation of your policy is subject to various components including future financing execution."

- Notes:

- i) This delineation is pertinent to a standard (from therapeutic, life style and occupation perspective) life.

- ii) The non-ensured profits (1) and (2) in above delineation are computed with the goal that they are steady with the Anticipated Financing Rate of Return suspicion of 4% p.a. (Situation 1) and 8% p.a. (Situation 2) separately. As such, in setting up this profit delineation, it is accepted that the Anticipated Financing Rate of Give back that LICI will have the capacity to procure all through the policy term of the policy will be 4% p.a. then again 8% p.a., as the case may be. The Anticipated Financing Rate of Return is not ensured.

- iii) The principle goal of the outline is that the customer can like the gimmicks of the item and the stream of profits in diverse circumstances with some level of quantification.

SECTION 45 OF INSURANCE ACT, 1938 :

- No policy of extra security might after the expiry of two years from the date on which it was effected, be brought being referred to by a back up plan on the ground that an announcement made in the proposal for protection or in any report of a therapeutic officer, or arbitrator, or companion of the guaranteed, or in any viable archive prompting the issue of the policy, was wrong or false, unless the safety net provider indicates that such explanation was on a material matter or smothered actualities which it was material to reveal and that it was deceitfully made by the policyholder and that the policyholder knew at the time of putting forth it that the expression was false or that it stifled certainties which it was material to uncover.

- Gave that nothing in this area should keep the guarantor from calling for confirmation of age whenever in the event that he is qualified for do along these lines, and no policy might be esteemed to be brought being referred to just in light of the fact that the terms of the policy are balanced on ensuing verification that the age of the life guaranteed was mistakenly expressed in the proposal.

PROHIBITION OF REBATES (SECTION 41 OF INSURANCE ACT, 1938 ) :

- 1) No individual might permit or offer to permit, either specifically or in a roundabout way, as an incitement to any individual to take out or recharge or proceed a protection in admiration of any sort of danger identifying with lives or property in India, any refund of the entire or a piece of the commission payable or any discount of the premium indicated on the policy, nor should any individual taking out or restoring or proceeding a policy acknowledge any refund, aside from such refund as may be permitted as per the distributed plans or tables of the guarantor: gave that acknowledgement by a protection operator of commission regarding a policy of life coverage taken out without anyone else present on his own life might not be esteemed to be acknowledgement of a discount of premium inside the significance of this sub-segment if at the time of such acknowledgement the protection executor fulfills the endorsed conditions creating that he is a true blue protection operator utilized by the safety net provider.

- 2) Any individual making default in conforming to the procurements of this segment might be culpable with fine which may stretch out to five hundred rupees.

- Note : "Conditions apply" for which please allude to the Policy report or contact our closest Extension Office.

“Insurance is the subject matter of solicitation”

Registered Office:

Life Insurance Corporation of India

Central Office, Yogakshema,

Jeevan Bima Marg,

Mumbai – 400021.

- 1. Eligibility Conditions and Other Restriction :

For Basic plan

- a) Base Essential Aggregate Guaranteed : Rs. 100,000

- b) Most extreme Fundamental Aggregate Guaranteed : No Restriction

- (The Essential Aggregate Guaranteed might be in products of Rs. 5000/ -)

- c) Least Age at section : 18 years (finished)

- d) Most extreme Age at passage : 50 years (closest birthday)

- e) Most extreme Development Age : 75 years (closest birthday)

- f) Least Policy Term : 15 years

- g) Most extreme Policy Term : 35 years

For LIC’s Accidental Death and Disability Benefit Rider

- a) Base Mishap Profit Aggregate Guaranteed : Rs. 100,000

- b) Most extreme Mischance Profit Aggregate Guaranteed :

- A sum equivalent to the Essential Aggregate guaranteed under the Fundamental Plan subject to the most extreme of Rs.50 lakh general point of confinement taking all current approaches of the Life Guaranteed under individual and gathering plans incorporating arrangements with inbuilt mishap profit brought with Extra security Organization of India and the Mischance Profit Entirety Guaranteed under the new proposal into thought.

- (The Mischance Profit Total Guaranteed might be in products of Rs. 5000/ -)

- c) Least Age at passage : 18 years (finished)

- d) Greatest Age at entrance : The spread could be decided on at any policy commemoration throughout the policy term yet before the policy celebration on which the age closer birthday of the Life Guaranteed is 70 years.

- e) Greatest spread stopping age : 70 years (closest birthday) or till the end of the Policy

- Term, whichever is prior.

- 2. Installment of Premiums:

- Premiums might be paid customarily at yearly, half-yearly, quarterly or month to month interims (through ECS just or through compensation findings) over the Policy Term.

- Then again, an effortlessness time of one logbook month however at the very least 30 days will be considered installment of yearly or half-yearly or quarterly premiums and 15 days for month to month premiums.

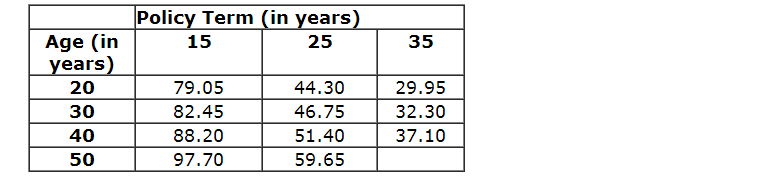

- 3. Sample Premium Rates:

- Following are some of the sample tabular premium rates (exclusive of service tax) per Rs. 1000/- Basic Sum Assured:

- 4. Mode and High S.a. Rebates: mode Refund:

- Yearly mode - 2% of Plain Premium

- Half-yearly mode - 1% of Plain premium

- Quarterly & Month to month mode - NIL

High Sum Assured Rebate:

Basic Sum Assured (B.S.A) Rebate (Rs.)

1, 00,000 to 1, 95,000 - Nil

2, 00,000 to 4, 95,000 - 1.50%o B.S.A.

5, 00,000 and 9, 95,000 - 2.50%o B.S.A.

10, 00,000 and above - 3.00%o B.S.A.

5. Revival:

- In the event that premiums are not paid inside the elegance period then the policy will slip by. A passed policy might be restored inside a time of 2 successive years from the date of first unpaid premium yet before the end of policy term on installment of every last one of unfulfilled obligations of premium together with enthusiasm (exacerbating half-yearly) at such rate as settled by the Enterprise occasionally, subject to submission of attractive confirmation of proceeded insurability.

- The Enterprise maintains all authority to acknowledge at unique terms, acknowledge at modified terms or decrease the recovery of a stopped policy. The recovery of stopped policy should produce results just after the same is sanction by the Partnership and is particularly conveyed to the Policyholder.

- Restoration of rider(s), if picked, will be considered alongside recovery of the fundamental policy and not in detachment

6. Paid-up Value :

- In the event that no less than three full years' premiums have been paid and any consequent premiums be not rightfully paid, this policy might not be wholly void, yet should proceed as a paid-up policy. The Fundamental Total Guaranteed under the policy might be lessened to such an entirety, called Paid-up Whole Guaranteed and should bear the same proportion to the Essential Aggregate Guaranteed as the premiums paid bears to the aggregate number of premiums payable i.e. Fundamental Entirety Guaranteed *(number of premiums paid/ number of premiums payable).

- This Paid-up Total Guaranteed alongside vested straightforward reversionary rewards, if any, is payable on the expiry of policy term or if there should arise an occurrence of former death. The reversionary rewards officially accumulated to the policy as on the date of paid-up will stay appended to the policy. A paid-up policy won't accumulate any further rewards. If there should arise an occurrence of death after the policy term Paid-up Whole Guaranteed will be paid.

- Rider(s) don't obtain any paid-up quality and the rider profits stop to apply, if policy is in lapsed condition.

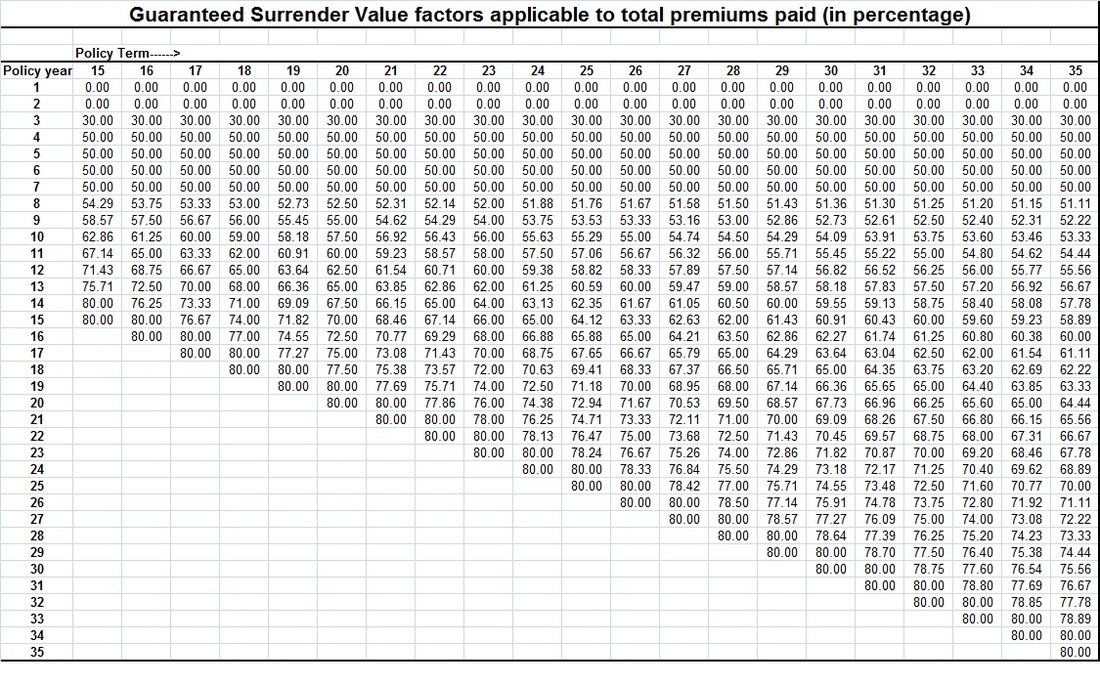

7. Surrender Value:

The policy could be surrendered for money gave atleast three full years' premiums have been paid. The Ensured Surrender quality throughout policy term might be a rate of aggregate premiums paid (net of service tax) barring additional premiums and premiums for riders, if selected. This rate will rely on upon the policy term and policy year in which the policy is surrendered and determined as beneath:

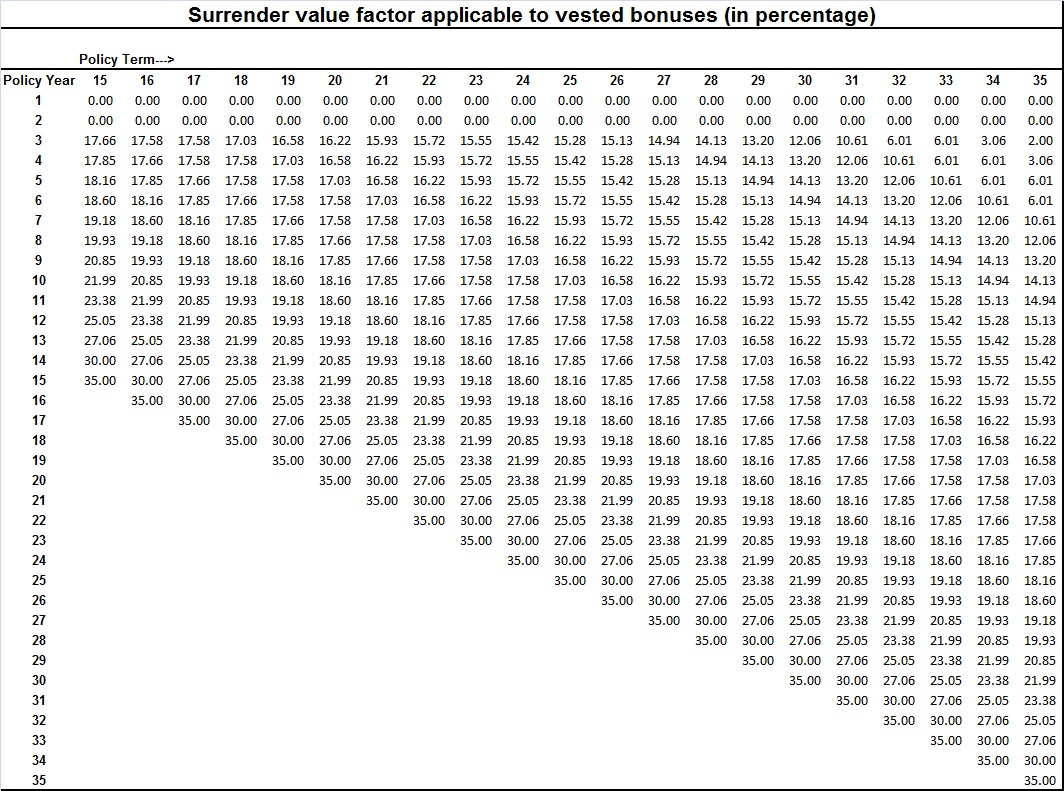

Moreover, the surrender estimation of any vested basic reversionary bonuses, if any, might likewise be payable, which is equivalent to vested bonuses increased by the surrender worth component appropriate to vested bonuses. These variables will rely on upon the policy term and policy year in which the policy is surrendered and defined as underneath:

- Enterprise might, notwithstanding, pay Uncommon Surrender esteem, on the off chance that it is more positive to the Policyholder.

8. Policy Loan:

Credit might be profited under the policy gave the policy has procured a surrender value and subject to the terms and conditions as the organization may define occasionally.

9. Taxes:

- Taxes including Administration Tax, if any, might be according to the Tax laws and the rate of tax should be as material every once in a while.

- The measure of tax according to the predominating rates might be payable by the Policyholder on premiums including additional premiums, if any. The measure of tax paid should not be considered for the count of profits payable under the plan.

10. Cooling-off period :

On the off chance that the Policyholder is not fulfilled by the "Terms and Conditions" of the policy may be come back to us inside 15 days from the date of receipt of the policy bond expressing the reasons of complaints. On receipt of the same the Partnership should scratch off the policy and give back where its due of premium saved in the wake of deducting the proportionate danger premium (for fundamental plan and rider(s), if any) for the period on spread, costs acquired on restorative examination, uncommon reports, if any and stamp obligation..

11. Exclusion:

- Suicide: - This policy might be void

- i. On the off chance that the Life Guaranteed (whether normal or crazy) submits suicide whenever inside 12 months from the date of beginning of danger and the Organization won't enliven any case under this policy but to the degree of 80% of the premiums paid barring any taxes, additional premium and rider premiums, if any, gave the policy is inforce.

- ii. On the off chance that the Life Guaranteed (whether normal or crazy) submits suicide inside 12 months from date of recovery, a sum which is higher of 80% of the premiums paid till the date of death (barring any taxes, additional premium and rider premiums, if any,) or the surrender worth, gave the policy is inforce, might be payable. The Enterprise won't captivate whatever viable claim under this policy.