LIC'S NEW MONEY BACK PLAN-20 YEARS (TABLE NO 820)

click here to buy online

click here To inquire

Life Insurance Corporation Of India Ltd. (LIC) Presents,

LIC's New Cash Back Plan-20 years is a partaking non-interfaced plan which offers an appealing consolidation of security against death all through the term of the plan alongside the intermittent installment on survival at tagged terms throughout the term. This extraordinary blend gives fiscal backing to the group of the expired policyholder whenever before development and knot aggregate sum at the time of development for the surviving policyholders. This plan additionally deals with liquidity needs through its credit office.

Profits:

Death profit: On death throughout the policy term gave the policy is in full constrain, death profit, characterized as aggregate of "Entirety Guaranteed on Death" and vested Straightforward Reversionary Bonuses and Last Extra Bonus, if any, might be payable. Where, "Entirety Guaranteed on Death" is characterized as higher of 125% of the Essential Total Guaranteed or 10 times of annualized premium. This death profit might not be short of what 105% of the aggregate premiums paid as on date of death.

The premiums said above prohibit tax, additional premium and rider premium, if any.

Survival Profits: if there should be an occurrence of Life Guaranteed making due to the end of the defined terms 20% of the Essential Aggregate Guaranteed at the end of each of fifth, tenth & fifteenth policy year.

Development Profit: if there should be an occurrence of Life Guaranteed surviving the stipulated date of development, 40% of the Essential Whole Guaranteed alongside vested Straightforward Reversionary Bonuses and Last Extra Bonus, if any, might be payable.

Investment in Benefits: The policy should take part in benefits of the Partnership and might be qualified for get Basic Reversionary Bonuses pronounced according to the knowledge of the Organization, gave the policy is in full constrain.

Last Extra Bonus might additionally be pronounced under the policy in the year when the policy results into a case either by death or development, gave the policy has rush to certain base term.

Optional Profit:

LIC's Coincidental Death and Incapacity Profit Rider: LIC's Unplanned Death and Handicap Profit Rider might be selected under an inforce policy whenever inside the premium paying term by installment of extra premium and the spread will be accessible all through the policy term gave the Policy is inforce to the full Whole Guaranteed as on date of mishap. If there should be an occurrence of unintentional death, the Mischance Profit Aggregate Guaranteed will be payable as lumpsum alongside the death profit under the essential plan. In the event of coincidental lasting incapacity emerging because of mishap (inside 180 days from the date of mischance), a sum equivalent to the Mishap Banquet Total Guaranteed will be paid in equivalent regularly scheduled payments spread in excess of 10 years and future premiums for Mischance Profit Whole Guaranteed and premiums for the segment of Fundamental Aggregate Guaranteed which is equivalent to Mischance Profit Entirety Guaranteed under the policy, should be waived.

Notwithstanding, on surrender of an inforce essential policy (which has obtained Surrender Worth) to which this rider is connected, an extent of extra premium charged in appreciation of spread after premium paying term should be discounted.

LIC's New Cash Back Plan-20 years is a partaking non-interfaced plan which offers an appealing consolidation of security against death all through the term of the plan alongside the intermittent installment on survival at tagged terms throughout the term. This extraordinary blend gives fiscal backing to the group of the expired policyholder whenever before development and knot aggregate sum at the time of development for the surviving policyholders. This plan additionally deals with liquidity needs through its credit office.

Profits:

Death profit: On death throughout the policy term gave the policy is in full constrain, death profit, characterized as aggregate of "Entirety Guaranteed on Death" and vested Straightforward Reversionary Bonuses and Last Extra Bonus, if any, might be payable. Where, "Entirety Guaranteed on Death" is characterized as higher of 125% of the Essential Total Guaranteed or 10 times of annualized premium. This death profit might not be short of what 105% of the aggregate premiums paid as on date of death.

The premiums said above prohibit tax, additional premium and rider premium, if any.

Survival Profits: if there should be an occurrence of Life Guaranteed making due to the end of the defined terms 20% of the Essential Aggregate Guaranteed at the end of each of fifth, tenth & fifteenth policy year.

Development Profit: if there should be an occurrence of Life Guaranteed surviving the stipulated date of development, 40% of the Essential Whole Guaranteed alongside vested Straightforward Reversionary Bonuses and Last Extra Bonus, if any, might be payable.

Investment in Benefits: The policy should take part in benefits of the Partnership and might be qualified for get Basic Reversionary Bonuses pronounced according to the knowledge of the Organization, gave the policy is in full constrain.

Last Extra Bonus might additionally be pronounced under the policy in the year when the policy results into a case either by death or development, gave the policy has rush to certain base term.

Optional Profit:

LIC's Coincidental Death and Incapacity Profit Rider: LIC's Unplanned Death and Handicap Profit Rider might be selected under an inforce policy whenever inside the premium paying term by installment of extra premium and the spread will be accessible all through the policy term gave the Policy is inforce to the full Whole Guaranteed as on date of mishap. If there should be an occurrence of unintentional death, the Mischance Profit Aggregate Guaranteed will be payable as lumpsum alongside the death profit under the essential plan. In the event of coincidental lasting incapacity emerging because of mishap (inside 180 days from the date of mischance), a sum equivalent to the Mishap Banquet Total Guaranteed will be paid in equivalent regularly scheduled payments spread in excess of 10 years and future premiums for Mischance Profit Whole Guaranteed and premiums for the segment of Fundamental Aggregate Guaranteed which is equivalent to Mischance Profit Entirety Guaranteed under the policy, should be waived.

Notwithstanding, on surrender of an inforce essential policy (which has obtained Surrender Worth) to which this rider is connected, an extent of extra premium charged in appreciation of spread after premium paying term should be discounted.

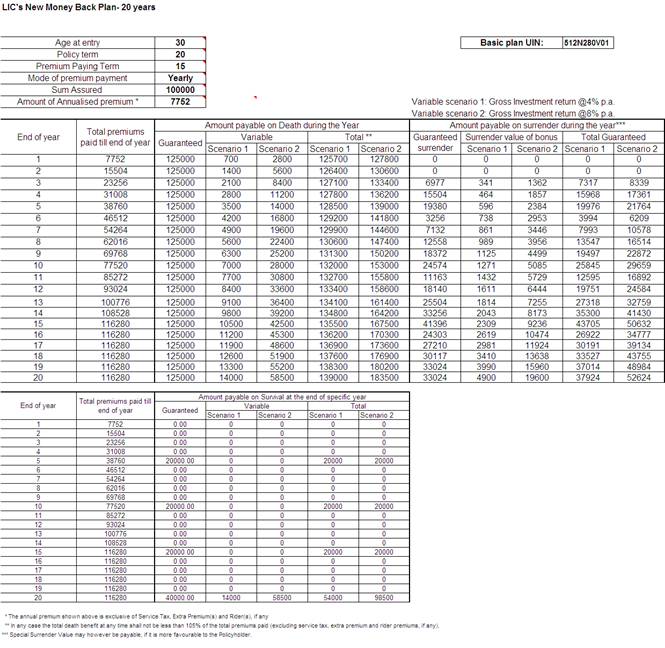

Benefit Illustration:

Statutory cautioning:

"A few profits are ensured and a few profits are variable with profits based for the future execution of your Guarantor carrying on life coverage business. In the event that your policy offers ensured returns then these will be unmistakably checked "ensured" in the outline table on this page. On the off chance that your policy offers variable profits then the representations for this page will indicate two separate rates of expected future financing returns. These accepted rates of return are not ensured and they are not the upper or lower cutoff points of what you may get again, as the estimation of your policy is subject to various components including future financing execution."

"A few profits are ensured and a few profits are variable with profits based for the future execution of your Guarantor carrying on life coverage business. In the event that your policy offers ensured returns then these will be unmistakably checked "ensured" in the outline table on this page. On the off chance that your policy offers variable profits then the representations for this page will indicate two separate rates of expected future financing returns. These accepted rates of return are not ensured and they are not the upper or lower cutoff points of what you may get again, as the estimation of your policy is subject to various components including future financing execution."

Notes:

No policy of disaster protection should after the expiry of two years from the date on which it was effected, be brought being referred to by a back up plan on the ground that an announcement made in the proposal for protection or in any report of a medical officer, or official, or companion of the guaranteed, or in whatever available record prompting the issue of the policy, was wrong or false, unless the guarantor indicates that such articulation was on a material matter or stifled realities which it was material to unveil and that it was deceitfully made by the policyholder and that the policyholder knew at the time of putting forth it that the expression was false or that it smothered certainties which it was material to reveal.

Gave that nothing in this segment might keep the back up plan from calling for evidence of age whenever in the event that he is qualified for do along these lines, and no policy should be esteemed to be brought being referred to simply in light of the fact that the terms of the policy are balanced on resulting verification that the age of the life guaranteed was erroneously expressed in the proposal.

PROHIBITION OF REBATES (SECTION 41 OF INSURANCE ACT, 1938):

No individual should permit or offer to permit, either straightforwardly or by implication, as an impelling to any individual to take out or replenish or proceed a protection in admiration of any sort of danger identifying with lives or property in India, any discount of the entire or a piece of the commission payable or any refund of the premium indicated on the policy, nor might any individual taking out or replenishing or proceeding a policy acknowledge any discount, aside from such refund as may be permitted as per the distributed plans or tables of the safety net provider: gave that acknowledgement by a protection executor of commission regarding a policy of extra security taken out without anyone else's input on his own life should not be considered to be acknowledgement of a discount of premium inside the significance of this sub-area if at the time of such acknowledgement the protection operator fulfills the endorsed conditions securing that he is a genuine protection operator utilized by the guarantor.

Any individual making default in agreeing to the procurements of this segment might be culpable with fine which may stretch out to five hundred rupees.

Note: "Conditions apply" for which please allude to the Policy archive or contact our closest Extension Office.

“Insurance is the subject matter of solicitation”

Registered Office:

Life Insurance Corporation of India

Central Office, Yogakshema,

Jeevan Bima Marg,

Mumbai – 400021.

Eligibility Conditions and Other Restrictions

Premiums could be paid consistently at yearly, half-yearly, quarterly or month to month mode (through ECS just) or through compensation conclusions over the term of policy.

Nonetheless, an elegance time of one month however at least 30 days will be took into consideration yearly, half-yearly, quarterly modes and 15 days for month to month mode of premium installment.

Sample Premium Rates:

Following are some of the sample tabular premium rates (exclusive of service tax) per Rs. 1000/- Basic Sum Assured:

- This delineation is pertinent to a standard (from medical, life style and occupation perspective) life.

- The non-ensured profits (1) and (2) in above delineation are ascertained so they are reliable with the Anticipated Financing Rate of Return presumption of 4% p.a. (Situation 1) and 8% p.a. (Situation 2) individually. At the end of the day, in setting up this profit delineation, it is accepted that the Anticipated Financing Rate of Give back that LICI will have the capacity to acquire all through the term of the policy will be 4% p.a. alternately 8% p.a., as the case may be. The Anticipated Financing Rate of Return is not ensured.

- The principle goal of the representation is that the customer can like the peculiarities of the item and the stream of profits in distinctive circumstances with some level of quantification.

No policy of disaster protection should after the expiry of two years from the date on which it was effected, be brought being referred to by a back up plan on the ground that an announcement made in the proposal for protection or in any report of a medical officer, or official, or companion of the guaranteed, or in whatever available record prompting the issue of the policy, was wrong or false, unless the guarantor indicates that such articulation was on a material matter or stifled realities which it was material to unveil and that it was deceitfully made by the policyholder and that the policyholder knew at the time of putting forth it that the expression was false or that it smothered certainties which it was material to reveal.

Gave that nothing in this segment might keep the back up plan from calling for evidence of age whenever in the event that he is qualified for do along these lines, and no policy should be esteemed to be brought being referred to simply in light of the fact that the terms of the policy are balanced on resulting verification that the age of the life guaranteed was erroneously expressed in the proposal.

PROHIBITION OF REBATES (SECTION 41 OF INSURANCE ACT, 1938):

No individual should permit or offer to permit, either straightforwardly or by implication, as an impelling to any individual to take out or replenish or proceed a protection in admiration of any sort of danger identifying with lives or property in India, any discount of the entire or a piece of the commission payable or any refund of the premium indicated on the policy, nor might any individual taking out or replenishing or proceeding a policy acknowledge any discount, aside from such refund as may be permitted as per the distributed plans or tables of the safety net provider: gave that acknowledgement by a protection executor of commission regarding a policy of extra security taken out without anyone else's input on his own life should not be considered to be acknowledgement of a discount of premium inside the significance of this sub-area if at the time of such acknowledgement the protection operator fulfills the endorsed conditions securing that he is a genuine protection operator utilized by the guarantor.

Any individual making default in agreeing to the procurements of this segment might be culpable with fine which may stretch out to five hundred rupees.

Note: "Conditions apply" for which please allude to the Policy archive or contact our closest Extension Office.

“Insurance is the subject matter of solicitation”

Registered Office:

Life Insurance Corporation of India

Central Office, Yogakshema,

Jeevan Bima Marg,

Mumbai – 400021.

Eligibility Conditions and Other Restrictions

- For Basic plan

- Minimum Basic Sum Assured : Rs. 100,000

- Maximum Basic Sum Assured : No Limit

- Minimum Age at entry for Life Assured : 13 years (completed)

- Maximum Age at entry for Life Assured : 50 years (nearest birthday)

- Maximum Maturity Age for Life Assured : 70 years (nearest birthday)

- Term : 20 years

- Premium paying term (PPT) : 15 years

- Least Mischance Profit Whole Guaranteed : Rs. 100,000

- Greatest Mishap Profit Entirety Guaranteed : A sum equivalent to the Aggregate Guaranteed under the Essential Plan subject to the most extreme of Rs.50 lakh Mischance Profit Total Guaranteed taking all current strategies of the Life Guaranteed under individual and gathering plans incorporating arrangements with in-manufactured mischance profit brought with Disaster protection Partnership of India and the Mischance Profit Whole Guaranteed under the new proposal into thought. (The Mischance Profit Aggregate Guaranteed should be in products of Rs. 5000/ -)

Premiums could be paid consistently at yearly, half-yearly, quarterly or month to month mode (through ECS just) or through compensation conclusions over the term of policy.

Nonetheless, an elegance time of one month however at least 30 days will be took into consideration yearly, half-yearly, quarterly modes and 15 days for month to month mode of premium installment.

Sample Premium Rates:

Following are some of the sample tabular premium rates (exclusive of service tax) per Rs. 1000/- Basic Sum Assured:

Mode and High S.A. Rebates:

Mode Rebate:

Yearly mode - 2% of Tabular Premium

Half-yearly mode - 1% of Tabular premium

Quarterly & Salary deduction - NIL

High Sum Assured Rebate:

Basic Sum Assured (B.S.A) Rebate (Rs.)

1, 00,000 to 1, 95,000 - Nil

2, 00,000 to 4, 95,000 - 2.00 %o B.S.A.

5, 00,000 and above - 3.00%o B.S.A.

The Organization claims all authority to acknowledge at unique terms, acknowledge at reexamined terms or decay the restoration of a ceased policy. The recovery of ended policy should produce results just after the same is endorsed by the Enterprise and is particularly imparted to the Policyholder.

Recovery of rider(s), if settled on, will be considered alongside restoration of the Essential Policy and not in seclusion.

2. Paid-up Value:

In the event that no less than three full years' premiums have been paid and any ensuing premiums be not properly paid, this policy should not be wholly void, however might proceed as a paid-up policy. The Essential Entirety Guaranteed under the policy should be diminished to such an aggregate, called Paid-up Total Guaranteed and might be equivalent to [(number of premiums paid/ Aggregate Number of premiums payable) x Fundamental Whole Assured] less Aggregate sum of survival profits effectively paid under the policy.

The policy so diminished might from there on be free from all liabilities for installment of the premiums, however should not be qualified for take part in future benefits. Nonetheless, the vested Basic Reversionary Bonuses should stay appended to the diminished paid-up policy.

Despite the profits accessible under a completely inforce policy, on account of a diminished paid up policy, no survival profits might be payable and the paid-up quality alongside the vested Straightforward Reversionary Bonuses, if any, should be payable just in irregularity entirety on the expiry of policy term or death of life guaranteed, if prior.

Rider(s) might not procure any paid-up quality and the rider profits stop to apply, if policy is in passed condition.

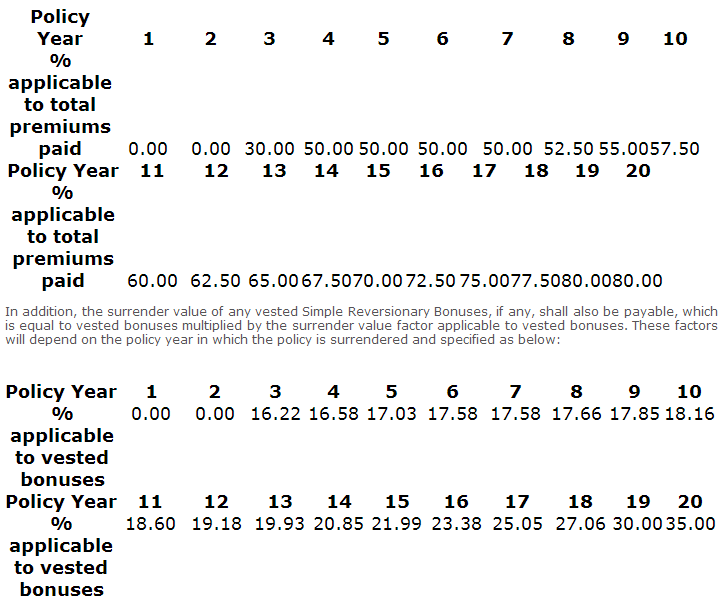

3. Surrender Value:

The policy can surrendered for money gave atleast three full years' premiums have been paid. The Ensured Surrender esteem should be rate of aggregate premiums paid (net of administration tax) barring additional premiums and premiums for riders, if picked less any survival profits effectively paid. This rate will rely on upon the policy year in which the policy is surrendered and defined as beneath:

Mode Rebate:

Yearly mode - 2% of Tabular Premium

Half-yearly mode - 1% of Tabular premium

Quarterly & Salary deduction - NIL

High Sum Assured Rebate:

Basic Sum Assured (B.S.A) Rebate (Rs.)

1, 00,000 to 1, 95,000 - Nil

2, 00,000 to 4, 95,000 - 2.00 %o B.S.A.

5, 00,000 and above - 3.00%o B.S.A.

- Revival:

The Organization claims all authority to acknowledge at unique terms, acknowledge at reexamined terms or decay the restoration of a ceased policy. The recovery of ended policy should produce results just after the same is endorsed by the Enterprise and is particularly imparted to the Policyholder.

Recovery of rider(s), if settled on, will be considered alongside restoration of the Essential Policy and not in seclusion.

2. Paid-up Value:

In the event that no less than three full years' premiums have been paid and any ensuing premiums be not properly paid, this policy should not be wholly void, however might proceed as a paid-up policy. The Essential Entirety Guaranteed under the policy should be diminished to such an aggregate, called Paid-up Total Guaranteed and might be equivalent to [(number of premiums paid/ Aggregate Number of premiums payable) x Fundamental Whole Assured] less Aggregate sum of survival profits effectively paid under the policy.

The policy so diminished might from there on be free from all liabilities for installment of the premiums, however should not be qualified for take part in future benefits. Nonetheless, the vested Basic Reversionary Bonuses should stay appended to the diminished paid-up policy.

Despite the profits accessible under a completely inforce policy, on account of a diminished paid up policy, no survival profits might be payable and the paid-up quality alongside the vested Straightforward Reversionary Bonuses, if any, should be payable just in irregularity entirety on the expiry of policy term or death of life guaranteed, if prior.

Rider(s) might not procure any paid-up quality and the rider profits stop to apply, if policy is in passed condition.

3. Surrender Value:

The policy can surrendered for money gave atleast three full years' premiums have been paid. The Ensured Surrender esteem should be rate of aggregate premiums paid (net of administration tax) barring additional premiums and premiums for riders, if picked less any survival profits effectively paid. This rate will rely on upon the policy year in which the policy is surrendered and defined as beneath:

- Company might, be that as it may, pay Exceptional Surrender esteem, on the off chance that it is more ideal to the Policyholder.

- Policy Loan:

- Taxes:

- Cooling-off period:

- Exclusion:

- Taxes including Administration Tax, if any, should be according to the Tax laws and the rate of tax might be as material occasionally.

- The measure of tax according to the predominating rates should be payable by the Policyholder on premiums including additional premiums, if any. The measure of tax paid might not be considered for the count of profits payable under the plan.

- On the off chance that the Life Guaranteed (whether rational or crazy) submits suicide whenever inside 12 months from the date of beginning of danger and the Partnership won't amuse any case under this policy but to the degree of 80% of the premiums paid barring any taxes, additional premium and rider premiums, if any, gave the policy is inforce.

- On the off chance that the Life Guaranteed (whether rational or crazy) submits suicide inside 12 months from date of restoration, a sum which is higher of 80% of the premiums paid till the date of death (barring any taxes, additional premium and rider premiums, if any,) or the surrender worth, gave the policy is inforce, might be payable. The Enterprise won't enliven any viable claim under this policy

BELOW IS THE PRESENTATION, DOWNLOAD TO KNOW EASILY

| new_money_back_plan_-820.pptx |